We always talk about retirement in Singapore and the projected expenses that we need to reach financial freedom. I set out on my journey with a target of having a passive income of S$3000 per month by the time I am 40 to cope with the rising cost of living in Singapore and possible inflation of my standard of living.

Now that I am 28 officially, my goals still stand with similar projections.

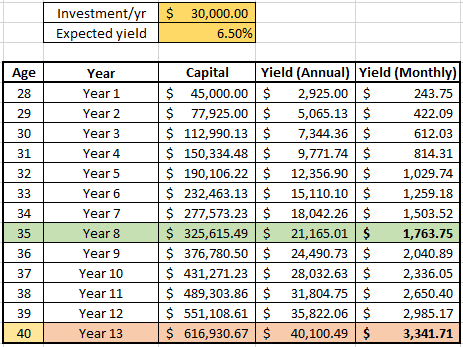

All I need is S$616,930.67 with a 6.5% annual yield to reach my goal.

Sounds easy? Of course not. That 600-odd thousand amount is the amount of money I have to have in my investment instruments ALONE. All the money I have in my CPF or emergency funds, or even war chest to be specific enough should not count in that amount.

Based on those numbers, I also have to pump in S$30,000 of fresh funds per year. That is not a small amount at all, and barely leaving me any other money for additional savings or other purposes.

But recently, I was introduced to another solution to reach retirement much faster. How fast you say?

On the same projections, it’ll quicken my retirement plans by 5 years. Which means that I can retire by 35.

The question that I want to ask myself is, what if I could retire overseas?

Well, it may not be the ideal solution for everyone, but it’s worth the consideration. And I’m pretty sure that there are many Singaporeans already doing this.

Now, when we discuss retirement, we start by thinking of standard of living firstly, and then how this S.O.L is being inflated over time. And then we decide how much money do we really need over life expectancy. Simple math, really, once you get down to it and your finances.

A close colleague (and friend) of mine is from the Phillipines and I got the chance to work very closely with him over the past year.

Naturally, me being Miss Niao, asked him what were his plans for retirement.

Since he is a Permanent Resident in Singapore, he has the CPF as a component for his retirement plans.

He also has a HDB which he is financing using his CPF funds and some cash.

Does he have plans to go back to Phillipines to retire? Yes, of course.

But how much does he need? I got a rough breakdown of expenses from him and some numbers from the Internet to justify the S.O.L in Phillipines.

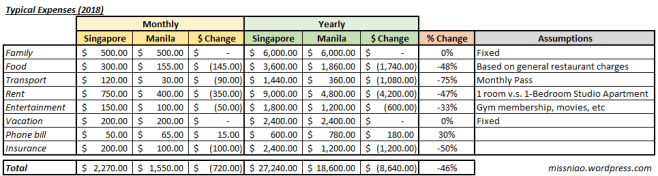

The Comparison

Let’s compare this to my own S.O.L here in Singapore and the S.O.L of a city area in Manila.

I’ll try to be as accurate as I can, with the discretion of Google.

As you can clearly see, there is a reduction of 46% based on total expenses. Plop those numbers back into the investment table:

As you can see, with an initial capital of $45,000 and yearly fresh funds of $30,000, at a 6.5% yield, one can survive off her passive income at the age of 35 in the Philippines, with more than enough to spare.

The capital that you need to fork out from your pocket(s) is almost half at only S$325,615.49.

And one who chooses to retire in Singapore can only do so 5 years later.

In addition, I do believe that it is not difficult to get a retirement visa in the Philippines as long as you have money – as how it usually works everywhere else in the world.

So, what’s stopping me?

Now of course, these are just very rough figures and we barely have taken additional precaution to increasing expenses due to inflation and GDP.

But what’s really stopping me is that I have commitments in Singapore that I can’t throw aside by packing my bags one day and decide that I want to semi-retire/retire in Philippines.

And a lot of other unforeseen possible scenarios on how my life might pan out in the next few years.

For example, I could have Singaporean kids who I would prefer to educate in Singapore being Singaporean myself.

I also have to rent an apartment in the Philippines. Foreigners are not allowed to own any asset unless a Filipino has ownership of at least 60% of the asset.

It would also be an entirely new culture that I have to adapt to, although the adjustment is very subjective and I might end up liking one over the other.

Nevertheless, as long as the possibility is open, I might consider it as long as the circumstances allow me to.

The ability to retire at Age 35 is both tempting and enticing.

What about you?

I know of a few colleagues who have plans to return back to their home country to retire, Malaysia being top of the list since it is only across the borders of Singapore.

But rarely of Singaporeans wanting to leave our sunny island, despite a bunch of us having the talent of complaining about almost everything about it.

Do you know of anyone that plans to live outside or Singapore, or is already doing it?

Or maybe you are one of them, contemplating on this option.

Share your views in the comments below. I would love to hear them.

In the meantime, I wish all readers a Merry Xmas and a Happy New Year in advance!

Miss Niao xoxo

Would I consider? Yup, of course.

I say, take it for a trial run. Live overseas in countries with slightly lower cost of living, such as Thailand for the resort lifestyle, or even Taiwan if we prefer Chinese speaking population. In addition to a (dividend-producing) portfolio, we can rent out our HDB apartment (if we have one) for that added income buffer.

With two streams of almost-passive income secured, explore a third active stream, if you prefer, in remote working opportunities – it isn’t that hard to come by these days. I’m not sure about you, but I see myself “being useful” in some capacity so this isn’t an issue for me at all.

A trial run is also an excellent opportunity to experience the problems of being away from our home country! 🙂

LikeLiked by 1 person

Yes I totally agree with creating more income streams to fund your retirement. I guess that’s what it’s all about – financial independence!

And it doesn’t matter where in the world you decide to pursue this in the end, as long as you can find ways to cover your expenses without “actively” working 🙂

LikeLike

Cost of living is the more appropriate term to use.

I intend to retire in Australia, UK or NZ.

I save 100% of my salary or 50% of my family income. We budget our expenses and invest the rest in stocks since I am risk averse. We have a kid and trying for another.

My short term target is for my cash investment account to hit $500k by 2021.

LikeLiked by 1 person

Wow that’s pretty impressive! I don’t know anyone who has kids and being able to save 100% of their salary apart from financial bloggers, I suppose. You are doing very well. Hope that you can achieve your goal!

LikeLike

Hello, I am doing my trial run now in Thailand. I am 43, will be here 2 year’s total and currently 1 half years here already.

I must say I even more cheapskate, my budget is 1k a month.

To adapt, I am learning Thai. I am a fair to dark skin Chinese.

What is your skin colour? I am not trying to be funny, but unless you are dark skin like a a chao tar roti, avoid the Philippines. Wherever you go, you must have the ability to blend in.

I did my first RTW when I was 35 and at same time studied our neighbors to see which country more suitable and comfortable for blending in.

I am still researching which visa, if need, is more suitable in Thailand. Unfortunately I started my shopping already, 3 bikes,1 car, 1 studio at last count, hahaha.

LikeLiked by 1 person

Oh wow! I know of a friend who plans to go to Thailand too for his retirement, as his wife is a Thai.

Then again, I was thinking more along the lines of dating a Filipino lol and it’ll probably provide me more reason to live there.

I am dark skinned naturally too, despite being Chinese. But not chao tar lol. I think I could blend well in other surrounding countries.

Glad you’re doing well in your retirement. 🙂

LikeLike

I think you will get $500,000 by 35. I think its good to have plans like this. It is likely what you will do is eventually different. But as long as you have that net worth, you have a lot of ways you could go. I still think Singapore could be cheaper than that.

LikeLike

$500,000 at 35! I think that’s very ambitious. I will probably be at the $400,000+ at most according to my own calculations.

That is true. As long as money is on the table, our doors are more open.

I agree, but for a more worst case scenario I blew the figures up 😀

LikeLike

Hi Ms Niao,

I think that you should be able to hit the said networth by 35 or 40. Having stated this comment, you may want to note that it might not be necessary to achieve the stated networth. I feel that the math is moot. You can consider reducing the expense further and hence the required networth will be lesser taking consideration of the reduced expenses. It’s all up to the flexibility and I believe that all people can exercise such flexible approach provided that they are willing to put it to action.

My two cents worth of views.

WTK

LikeLike

I agree that the figures can be reduced, but as an engineer by nature I considered more worst case scenarios 😀

Yes, we should be flexible in our planning. Life is not going to be as rigid as we think it will be.

LikeLike

Hi. Ms Niao. Totally agree with your views. Flexibility is the way to go. I am now at the age in which you target to be FIRE. I wish you all the best and believe that you will be able to retire before the age of 40. Keep the belief and enjoy the present moment.

LikeLiked by 1 person