BF and I were having a Whatsapp conversation one day.

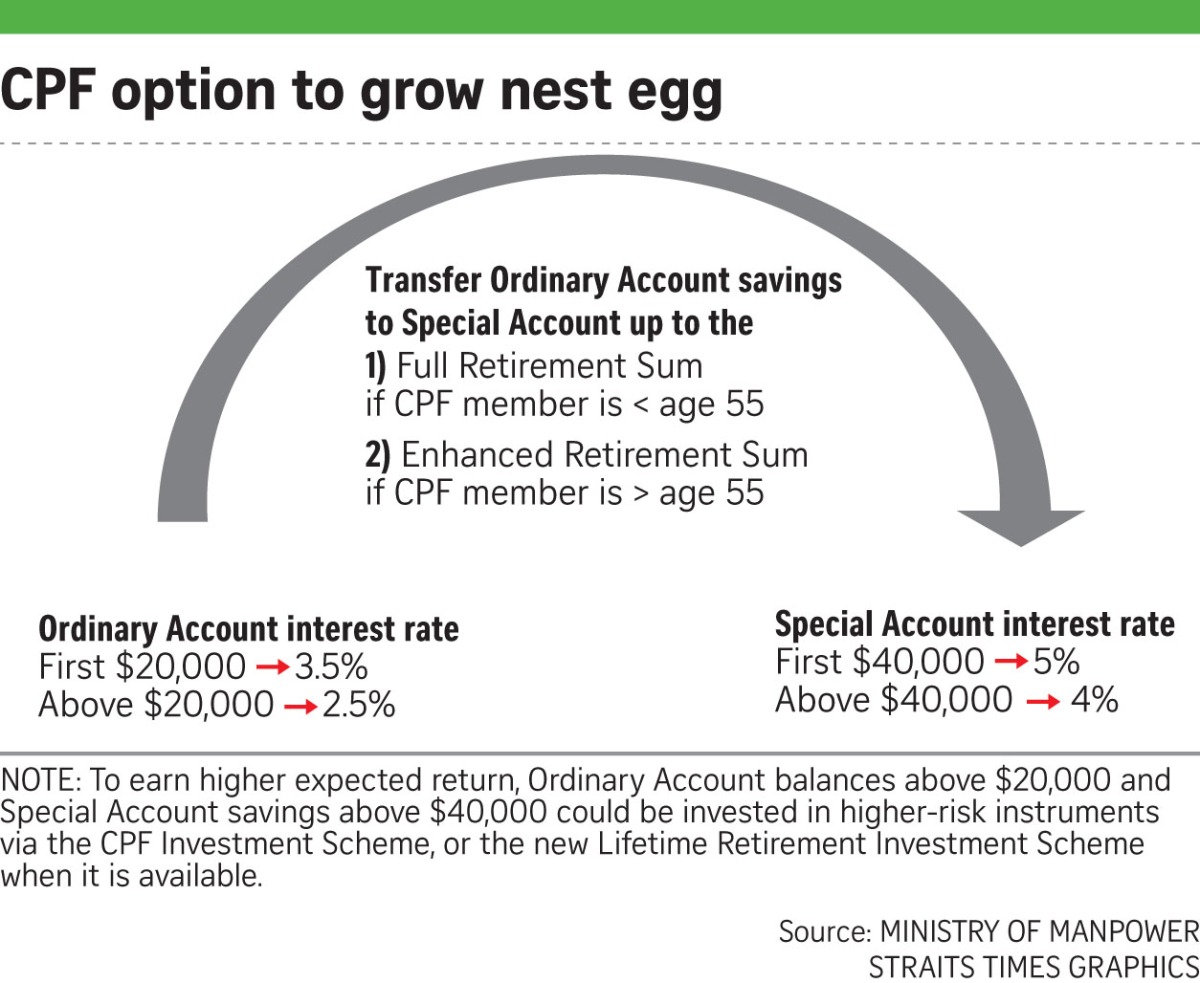

Me: BB, I read that got people transfer their funds from OA to SA, maybe we should do it leh! Got higher returns.

BF: Huh is it? Never hear before leh. Then transfer already can transfer back anot?

Me: Er, don’t think so leh.

BF: Then next time want to buy house how?

Me: Er….

BF: Better check first. Then decide what we want to do.

Me: Okok, I read more…

We continued discussing even further and eventually we decided that there was too much to discuss. After gathering all the information I have found online, I have arrived at a few conclusions.

1) The CPF website is super chapalang (disorganized).

In order to get a specific piece of information, I needed to click a few links before reaching my destination. Sometimes even go one big round and then end up at the place where I started. It is like weaving through a maze. Haiyo.

2) Once you master the CPF system, it is hard to forget it.

In fact, it would seem like everything would fall into place. You will automatically know what you need to do in order to use the CPF to your advantage.

3) Do not just limit your knowledge to the CPF website.

Information about CPF is boundless. Knowledge is power, but applying your knowledge is a different thing entirely. Do your research and see what people are doing with their CPF accounts. And adopt the approach that would work best for you.

That being said, on the same weekend, BF and I sat down in front of the PC to analyze the CPF system. Funny how other couples go for movie dates but ours is to study the CPF. Lol.

I’ve opened a new category in my blog named as “The CPF system”. Subsequent blog posts about the CPF will be placed in this category. So if you want to know more about the CPF and how I utilized this to control my finances, please click here. I hope that it would be able to give you some insight and you’ll be able to find what you need.

Thanks for reading!

Miss Niao xoxo