Many of my friends around me think that I have this secret obsession with money. They know that I track my expenses on a daily basis and can never understand how I can bring out the time to do so. The reason is simple – I make it a priority in my life to achieve financial independence, and there is no other (better) way I know to achieve that – by reducing my expenses and increasing my income. And the only way that I can reduce my expenses is to know what I’ve been spending my money on.

I don’t want any of that precious stuff to go to waste.

Everyone does their budgeting in their own way. The ultimate goal for me is to save as much as I can, without sacrificing some of the values I have in life. Being able to save, really, is one of the basic stuff that you have to do in order to increase your net worth. And then once you have money, you can use it to make more money.

For 2018, I have decided to split my financial report into two sections.

- Income, and the different sources of income that I have and…

- Expense, both fixed and variable.

It’s pretty similar to a balance sheet as you would see in any annual report, and I’m wondering if reading too many annual reports has diverted me unconsciously into this style of reporting lol. But anyway, it is easier this way because I do have an offline Excel chart to do some simple calculations on how much I save every month and my savings rate.

Also, I try to keep my categories as lean as I can to prevent any confusion in the later stages when I have more income streams and expenses of different areas.

Income

This year, I have employed more revenues of income from different sources.

1. Salary

The main source of income is of course, my 9-to-6 job which I hold dearly to. It gives me a set of fixed income until the next year’s expected increment. And it is also from here where majority of my savings come from.

This is also the only income where I have to physically work for money.

2. Dividends

The second biggest component of my income comes from dividends, having starting my journey in 2017. This is considered my passive income and will be used to calculate to show how far I am from financial independence.

You can read more about my dividend income in my 2018 portfolio update.

3. DBS Multiplier Account

I was a bit hesistant in doing this initially, but I finally pulled the plug to make the switch from the my OCBC 360 account and opened a DBS Multiplier Account for higher yield in my savings account.

First off, it is easier to track the criteria. You basically only need to credit your salary and charge everything to ONE DBS/POSB CC.

Secondly, you can achieve the investment criteria by linking up your CDP account or invest your funds using DBS Vickers.

I have been tracking the interest that I have been getting every month, and it really adds up to something significant at the end of the year. I also consider this source as a passive one.

4. Singapore Savings Bond

As the interest rates of SSBs have been steadily rising and even offered better rates than the FDs based on first year yields, it would be silly of me to not park some of my spare funds with a AAA rated government bond, in lieu of future use.

The bonds have started giving me some interest from the end of 2018, and serves as another small component of my passive income sources.

5. Other miscellaneous income

…which is not very significant to mention.

Expenses

I burst my initial budget of $18,000 which I optimistically set for my financial goals by a whooping 43%! I am honestly still surprised at the figures as I am typing them right now, but there were many reasons why I had to… and somehow I feel that these reasons are rather justifiable for my final expenses of $25,739.19 for the year of 2018. If you think about it, that’s half a quarter of a $100,000, which I painstakingly managed to save after 4-5 years of working full-time. It amounts to an average of $2,145 per month.

That is actually quite a huge amount considering that it is only slightly lesser than my starting take-home pay of $2,240.

My final savings rate is around 60~65% of my total income.

Not very impressive, but nonetheless nothing I spent on that I regretted too much about.

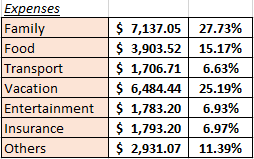

My expenses breakdown are as below:

Fixed Expenses

Family, transport and insurance categories are pretty much fixed expenses. They are unavoidable when due and I always make sure that I allocate enough funds every month to pay them.

Variable Expenses

The biggest variable here are vacation expenses which I have spent 1/4 of my expenses on! This was mainly due to the fully paid expense holiday that I sponsored my mum and grandmother to, and a few other pockets of trips throughout the year. You can read about some of my budget travelogues here and here.

Entertainment and Others contribute to 18%, and these categories include wedding ang baos, movies, birthday gifts and other chill-out expenses.

In 2019, fortunately, I believe that I will be spending a lot lesser on vacations and try to stick to a stricter budget. The only category that I will try to maintain or increase will be food, which is at a surprisingly low 15%. Eating out can be reasonably cheap in Singapore too!

Alternatively, I always wonder if I can skip more weddings :p.

How far am I from Financial Independence?

Based on my Total Passive Income (excluding CPF interest) over Expenses, the percentage is 10.97%.

As compared to annualized calculations in 2017 of 3.71%, I would say that I’m a few more steps closer to FI!

Budgeting for 2019

To keep things simple, I only have numbers to describe my goals this year.

My income goal

- Increase total income by 10%.

- Increase passive income from dividends to $4,500

My expenses goal

- Reduce total expenses to $20,000 (I can do it!)

Overall goal

- Increase Total Passive Income over Expenses to 20%

- Increase Savings Rate to 75%

Ambitious, perhaps. But it’s just a goal and I will review them quarterly, like in 2017.

I wish that you had a great reporting year in 2018. Let’s press on for 2019 and continue to build wealth together here!

Miss Niao xoxo.

lol i guess we have the same obsession in calculating daily

LikeLike

Lol ikr. It’s always satisfying to know that you’re doing things to increase your net worth.

LikeLike

Sponsoring a trip for your mom and grandmother may have busted your spending budget this year, but it has created memories for them to hold dear.

LikeLike

I think that they did enjoy the trip! 😉

LikeLike

Sounds like a great plan. All the best

LikeLike

Thank you, and the same to you!

LikeLiked by 1 person

well done.

was the 60~65% saving rate all cash saving?

LikeLike

Thanks!

No, of course not. It is based on total income 🙂

LikeLike

Hi Ms Niao,

As long as the percent relating the passive income over the expense is increasing over the year, you are inching towards the promised land of FI in which you have the option of RE. Keep increasing the saving and reducing the expense is the way to a greater compounding effect.

I wish you a shorter time to FI.

WTK

LikeLike

Interesting, I have forgot to also calculate the number of years that I need to reach that magical 100%. Thanks for your comment!

LikeLike

Interesting! Love you Miss Niao

LikeLiked by 1 person

Hi Miss Niao,

Great Job on becoming 7.26% closer to financial independence! If we extrapolate this increment rate, you are very likely to reach before age 40.

LikeLiked by 1 person

Thank you TBWP. I hope so, but due to certain circumstances I think it would be difficult!

LikeLike

Hi Miss Niao,

Will you be willing to share the excel you use to tabulate your expenses? Want to take a look at how you categorise them. I was trying to start my own excel to track my expenses and my expenditure to income ratio but Im not sure how to categorise them after lumping them all in one excel.

LikeLike

Sure! I’ll make a post about it over the weekend. Check my blog out again at the end of this week.

LikeLike